African Development Bank Group and Eritrea strengthen partnership for growth

The African Development Bank Group and Eritrea on Friday strengthened their partnership to support the country’s growth and place it

Eritrea: The African Development Bank Board approves US$49.92 million to Build a 30 MW Solar Photovoltaic Power Plant in Dekemhare

Financing Approval date 1 March 2023 Project name: Dekemhare 30-megawatt photovoltaic solar power plant project in Eritrea. Amount: US$ 49.92

Danakali to sell stake in flagship Colluli potash project in Eritrea

Australia’s Danakali (ASX: DNK) is selling its 50% stake in the Colluli potash project in Eritrea, Africa, almost 13 years after partnering with the

Eritrea Economic Outlook

Macroeconomic performance and outlook

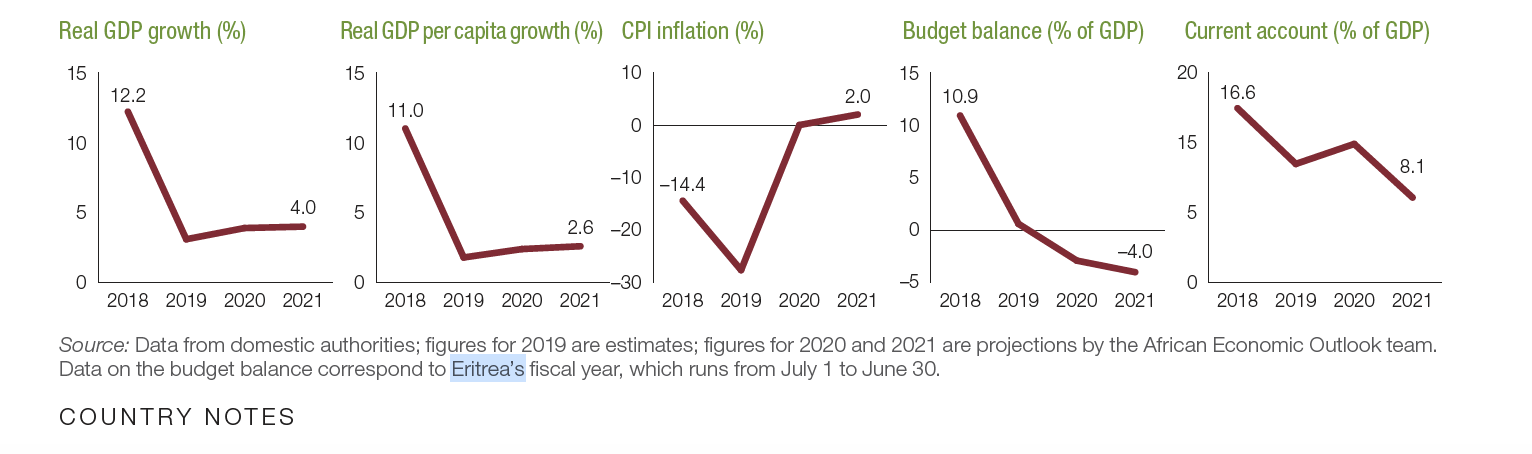

Real GDP is estimated to have fallen to 3.1% in 2019 due to subdued final demand of investment and exports. On the supply side, mining and agriculture remained the dominant contributors to real GDP growth. On the demand side, government investment in infrastructure— notably in energy, roads, and irrigation— underpins growth. The economy has experienced a persistent fall in consumer prices for three consecutive years (2017– 19), down 13.3% in 2017, 14.4% in 2018, and an estimated 27.6% in 2019. Deflation is structurally driven by the low prices of imported consumer goods supported by contraband trade and an overvalued exchange rate (by 14.9% in real effective terms). The fiscal balance is estimated at 0.6% of GDP in 2019, down from 10.9% in 2018, and domestic credit is estimated to grow at 1.4%. With total debt at 248.9% of GDP in 2019, Eritrea is already at high risk of debt distress, reducing its debt carrying capacity. While the bulk of this debt is domestic, external debt is estimated at 64.4% of GDP. The current account surplus fell to 11.3% of GDP in 2019, largely reflecting a drop in net exports. In 2019, gross international reserves are estimated to cover 3.1 months of imports, up from 2.7 months in 2018, but are less than adequate to weather external shocks. Tailwinds and headwinds The economic outlook is positive, with real GDP growth projected to increase to 3.9% in 2020 and 4.0% in 2021. Per capita income is expected to grow from 1.8% in 2019 to 2.6% in 2021. Underpinning this outlook are the removal of UN sanctions, the dividends from continuing the September 2019 peace and friendship agreement with Ethiopia, and the cessation of hostilities with Djibouti. This has paved the way for the re-engagement of various international organizations that will support various sectors of the economy. There is confidence in the country’s macroeconomic outlook, particularly the possibility for embarking on financial reforms. The main opportunities are in mining, tourism, and agriculture. Increased investment in copper, zinc, and Colluli potash is expected to drive growth in mining. The Africa Finance Corporation and the Africa Exim Bank will jointly finance potash production. And investors from Italy and the Eritrean diaspora have expressed interest in developing the islands and coastlines, which would boost tourism. Agriculture is attracting development partner investments in irrigation, microcredit, and alternative livelihoods. The Horn of Africa initiative is focusing on infrastructure and human development as drivers of growth. Debt distress could culminate in a drop in the sovereign rating and a rise in interest spreads, constraining growth. Given the dominance of state enterprises and their dependence on state financing, the spillover effects of sovereign debt on these enterprises could reduce output. Dependence on exports of gold and zinc and agricultural raw materials makes the country vulnerable to external shocks. The demand for Eritrea’s commodity exports could be reduced by sluggish growth in the global economy, particularly the key trading partners in Europe and the Far East. Vulnerability to climate shocks and delayed agricultural transformation have reduced agricultural productivity. Given the size and importance of this sector for food security and employment, lower productivity could constrain the potential contribution of agriculture (now 20% of GDP). Constraints on starting a business, dealing with construction permits, registering property, obtaining electricity, obtaining credit, and protecting minority investors increase financing costs and reduce returns on investment. Skill mismatches, poor roads, weak domestic finance, and inadequate information and communications technology also reduce the returns to investment and projected growth. The government is addressing skill mismatch by building capacity and developing appropriate curricula for technical and vocational education and training. Eritrea remains low on the Human Development Index, ranked 182 of 189 countries.

Danakali eyes finish line for Eritrea potash project

Eleven years after acquiring the project and 10 years after the first drill hole was sunk, Danakali (ASX: DNK, LSE: DNK) is

Danakali scores Eritrea nod for vast potash mine

Australia’s Danakali (ASX, LON:DNK) is closer to getting its Colluli potash project off the ground after the Eritrean Ministry of

AFC INVESTS US$150 MILLION IN THE ERITREAN COLLULI POTASH PROJECT

Lagos, 16 December 2019 : Africa Finance Corporation (“AFC” or the “Corporation”), the leading infrastructure solutions provider in Africa, announces

THE STATE OF ERITREA BECOMES AFRICA FINANCE CORPORATION’S 24TH MEMBER STATE

Investment Opportunities in Eritrea

On Tuesday, July 24, 2018, Corporate Council on Africa hosted a working group on Investment Opportunities in Eritrea, with guest